27 May, 2026

FY26: Market-leading growth without margin compromise.

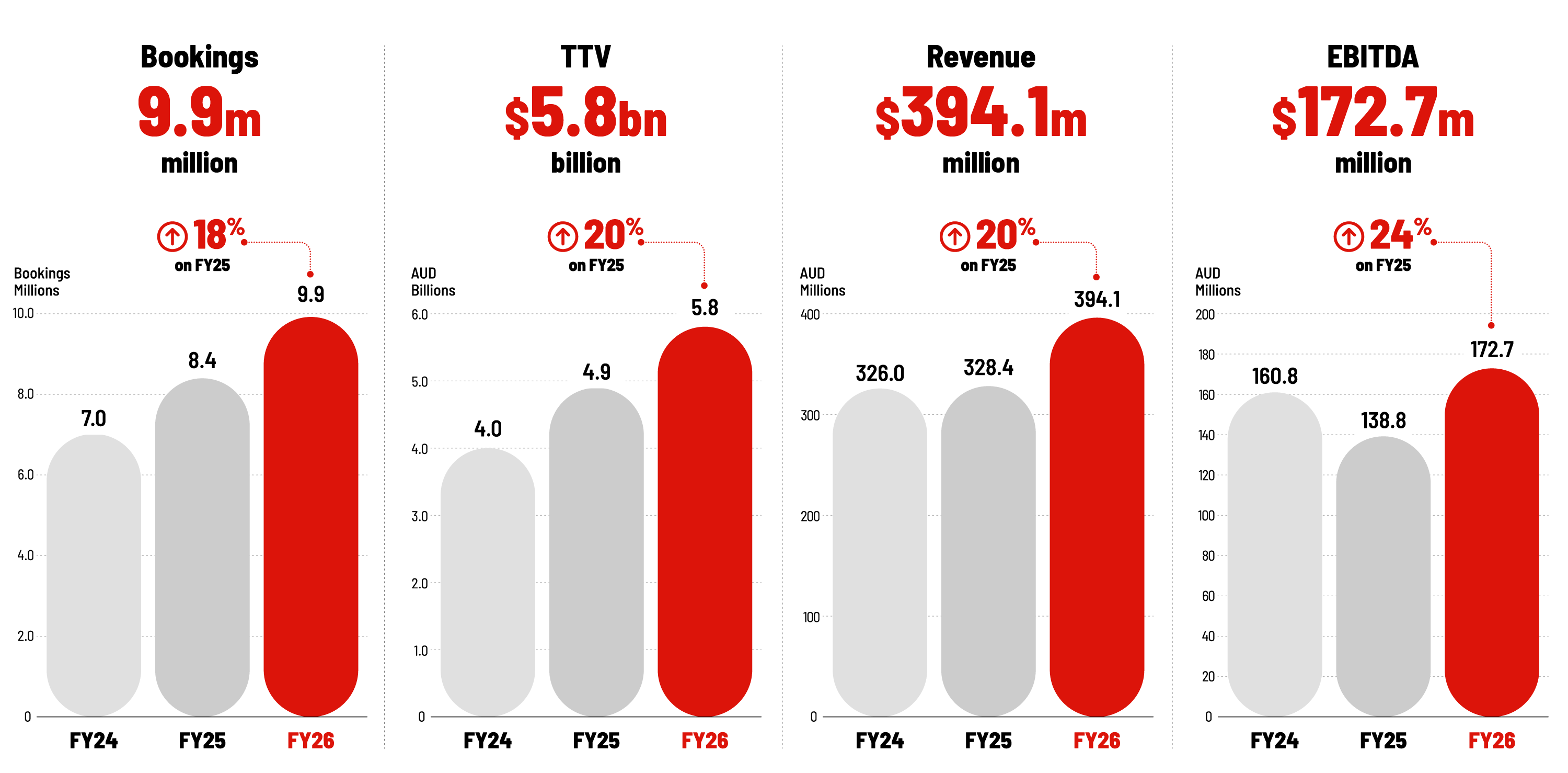

Web Travel Group today announced its financial results for the 12 months to 31 March 2026, with TTV up 20% to $5.8 billion, Revenue up 20% to $394.1 million and TTV margins 6.8%.

27 May, 2026

Web Travel Group today announced its financial results for the 12 months to 31 March 2026, with TTV up 20% to $5.8 billion, Revenue up 20% to $394.1 million and TTV margins 6.8%.

Web Travel Group’s results for FY26 saw Bookings, Total Transaction Value (TTV), Revenue, earnings before interest, tax, depreciation and amortisation (EBITDA), Net profit after tax (NPAT) and earnings per share (EPS) all up compared to FY25. Full details available in the Managing Director's Presentation, below.

FY26 Key Metrics: Bookings up 18% reflect significant organic growth in Americas and Europe; TTV up 20% in line with bookings growth, Revenue up 20% with TTV margins expanding & EBITDA up 24% reflecting operating leverage.

FY26 Key Metrics: Bookings up 18% reflect significant organic growth in Americas and Europe; TTV up 20% in line with bookings growth, Revenue up 20% with TTV margins expanding & EBITDA up 24% reflecting operating leverage.

WebBeds Bookings were up 18% compared to FY25 driven by significant organic growth in the Americas and Europe. Asia-Pacific (APAC) and Middle East & Africa (MEA) regions were both impacted by escalation of the conflict in the Middle East. TTV was up 20% in line with Bookings growth and Revenue was up 20% reflecting continued margin improvement. FY26 TTV margin was 6.8%, up from 6.7% in FY25 (on a like-for-like basis adjusting for the DMC business sold in April 2025, FY25 TTV margin was 6.6%). WebBeds FY26 Expenses were up 17% reflecting CPI increases and the re-inclusion of bonuses during the year, as well as the investment in hotel contracting resources announced last year. In EURO functional currency Expenses were up 10%. WebBeds EBITDA was up 24% reflecting operating leverage coming through.

After taking into account Corporate overheads of $24.3 million, FY26 Underlying Group EBITDA was up 23% on FY25. FY26 NPAT was $85.9 million up 8% reflecting the first full year of standalone costs since the Demerger. FY26 Underlying EPS was 23.8 cents, up 16% on FY25.

Commenting on the result, Web Travel Group Managing Director John Guscic said:

“FY26 was a terrific year for the WebBeds business. We continue to win share, TTV margins continue to improve, and our scalable business model is delivering higher operating leverage. WebBeds’ EBITDA margin remains world class.

We have been able to maintain our market-leading TTV growth rate with no margin pressure. WebBeds delivered $1 billion incremental TTV [1] this year at an improved margin compared with last year, demonstrating disciplined growth and margin resilience. This impressive result was delivered in an environment where the conflict in the Middle East placed downward pressure on Bookings and TTV in March 2026.

The key driver of our FY26 result was the outstanding performance of our Americas business which saw Bookings 41% higher than the previous year. Europe also performed well with Bookings up 19%. While APAC and MEA were both impacted by the conflict in the Middle East, both regions increased Bookings during the period. We continue to gain share by expanding our existing portfolio, winning new customers, enhancing supply sources, extending geographic reach and improving conversions. This is a direct result of the skill, dedication and focused execution from our teams around the world.

We continue to see exciting growth opportunities however the current trading environment remains uncertain. Trading conditions continue to be impacted by geopolitical instability in the Middle East particularly across MEA and parts of APAC. While the operating environment remains uncertain, we continue to demonstrate resilience across a number of key markets.

For the first 8 weeks of FY27 trading Bookings were up 6%, TTV was up 4% in constant currency and down 6% in Australian dollars compared to the same period last year. Americas and Europe continue to deliver growth but the conflict continues to have a material impact on MEA and, to a lesser extent, APAC. Importantly we continue to expect FY27 TTV margins of at least 6.5%, reflecting ongoing pricing discipline and resilience in the underlying business model.

While the duration and broader macroeconomic impacts of the conflict remain uncertain, we remain well positioned to benefit from any recovery in travel activity across affected regions and continue to expect long term growth in Bookings and TTV consistent with historical trends.”

[1] Excluding TTV from DMC operations sold in April 2025 to provide a like-for-like comparison of the underlying business

Commenting on recent capital management initiatives, Web Travel Group’s Chair Roger Sharp said:

“The conversion date for the Company’s $250 million Convertible Notes ended on 25 March 2026 and after balance date, all outstanding Notes were redeemed on 12 April 2026. Redemption was from a combination of existing cash and revolving credit facility. Following redemption, we continue to have strong liquidity based on working capital and undrawn credit lines, providing us with the flexibility to pursue any attractive M&A opportunities that might arise in the current economic climate.

The Board constantly evaluates a range of capital management opportunities. Our capital management priority is growth - organic and inorganic - supported by a conservative balance sheet that preserves optionality as market conditions evolve. Given the current level of geopolitical and economic uncertainty, at this time we believe it is appropriate to maintain a conservative balance sheet and prudent cash reserves.”

Further information on FY26 performance is set out in Web Travel Group’s FY26 Investor Presentation and Financial Report for the year ended 31 March 2026.

For more information of company performance, please visit the Web Travel Group Investor Centre website.

To be the most trusted, agile and value driven partner in our industry - powered by a culture where our people thrive, innovation flourishes, and our hunger to win delivers lasting impact for our customers.

Empower our people to deliver exceptional value through integrity, respect and relentless curiosity - challenging conventions, embracing change and working together to create superior outcomes for our customers.