Commenting on the result, Web Travel Group Managing Director John Guscic said:

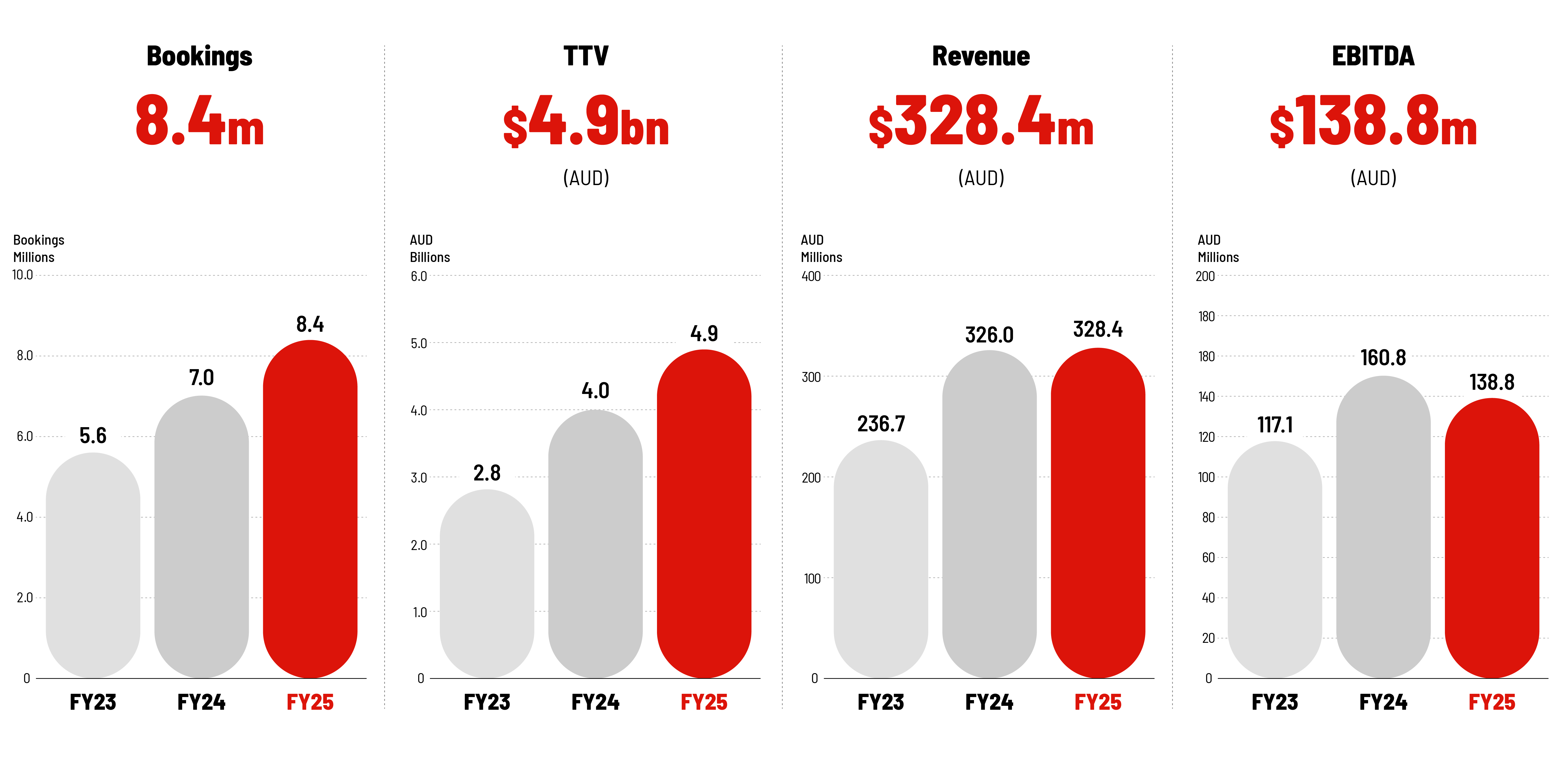

“Our significant TTV growth continued unabated during the year. At almost $5 billion, TTV is nearly double what it was before the pandemic, with our key growth markets of Asia-Pacific and the Americas now accounting for 53% of TTV, up from 31% pre pandemic. After events in the first half saw TTV margin expectations fall, margins stabilised in the second half and EBITDA for the full year was in line with expectations. WebBeds’ TTV growth rate is the highest of the global travel companies and at 42%, EBITDA margins remain world class.

We are confident TTV margins will be at least 6.5% for the medium term. Company-driven factors in the first half have been addressed and we are actively looking for opportunities to increase margins. Our focus is now on optimising supply mix. We are investing in directly contracted inventory, reengineering supply agreements and increasing the number of hotel contractors, particularly in Asia Pacific and the Americas. We are confident this will generate significant earnings growth in the short to medium term.

Post demerger the WebBeds business is repurposed, the team is reinvigorated and we are all focused on maintaining our market leading TTV growth rates, and driving economies of scale to deliver significant EBITDA growth by FY30.

We have had an exceptional start to FY26 trading with TTV up 37% and Bookings up 29% compared to the same period last year. We are targeting record EBITDA in FY26 and remain committed to delivering $10 billion TTV in FY30 at circa 50% EBITDA margins.”

Commenting on recent capital management initiatives, Web Travel Group’s Chair Roger Sharp said:

“In line with the Company’s objective to maximise shareholder value and reduce potential future dilution from the $250 million convertible notes due in April 2026, we completed a $150 million on-market share buyback in March 2025. Through the buyback and equity linked financial assets in place, collectively we have addressed approximately 88% of the potential future dilution from shares linked to the convertible notes.

While we are confident in the medium term outlook for the Company’s share price, given the current volatility of global equity markets, there is a risk note holders may choose to have the notes repaid in April 2026 instead of converting them to shares. We have therefore increased the revolving credit facility from $40 million to $200 million to provide ample liquidity to support this scenario.”

Further information on FY25 performance is set out in Web Travel Group’s FY25 Investor Presentation and Financial Report for the year ended 31 March 2025.